Attitudes begin to shift regarding monetary policy, economic growth, and stock prices

[ad_1]

This post was originally published on TKer.co

Stocks declined, with the S&P 500 falling 1.1% last week. The index is now up 6.5% year to date, up 14.4% from its October 12 closing low of 3,577.03, and down 14.7% from its January 3, 2022 closing high of 4,796.56.

Over the past two weeks or so, it seems attitudes have begun to shift favorably regarding monetary policy, economic growth, and the trajectory of stock prices.

1. The Fed acknowledges inflation is coming down 🦅

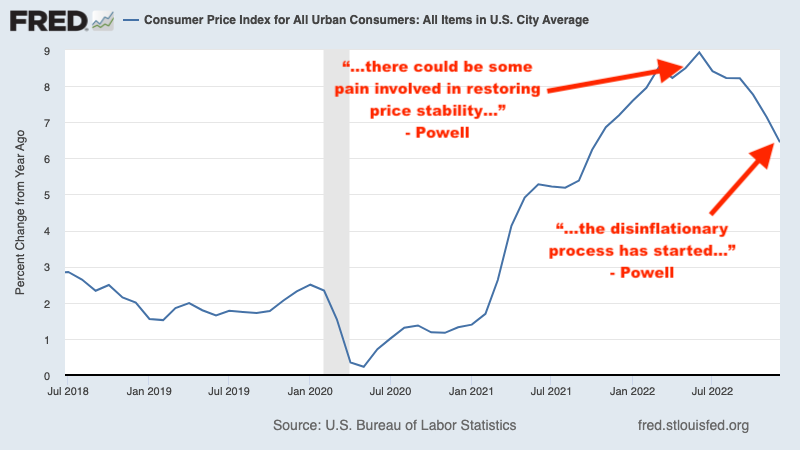

In May of last year, Fed Chair Jerome Powell warned “there could be some pain involved in restoring price stability.” A month later, we learned inflation was unexpectedly heating up again. And then on June 15, the Fed announced an eye-popping 75-basis-point interest rate hike, the largest increase the central bank made in a single announcement since 1994.

Back then, I explained how these dynamics presented a conundrum for the stock market as market beatings would continue until inflation improved in the Fed’s eyes.

Fast forward to February 1, following several months of cooling inflation data, when Powell said at the conclusion of the Fed’s monetary policy meeting: “We can now say, I think, for the first time that the disinflationary process has started. We can see that.“ (Emphasis added.)

“Powell cited the word ‘disinflation’ 13 times in this press conference,” Tom Lee, head of research at Fundstrat Global Advisors, wrote that day in a note to clients. “This is a major change in language and tone and shows that the Fed is now officially recognizing the growing disinflation forces underway. In [the December press conference], ‘disinflation’ was used ZERO times by Powell.”

This is a pretty big deal for the stock market, as prices tend to bottom in the weeks and months before major bullish developments. If this less hawkish tone from the Fed holds, then it’s possible the October 12 low for the S&P 500 was the beginning of the next bull market.

“In our view, Chair Powell is placing more weight on an ‘immaculate disinflation’ scenario, where inflation pressures subside without some softening in labor market conditions, including higher unemployment,” Michael Gapen, U.S. economist at BofA, wrote on Tuesday. “This stands in contrast to the Powell from Jackson Hole, Wyoming, last August, who leaned strongly into doing whatever it takes to bring inflation down and emphasized that inflation was unlikely to subside without some ‘pain’ in labor markets.”

As long as the inflation numbers continue to trend on the cooler side, the Fed seems likely to keep its less hawkish tone.

For more, read: TKer’s 2022 word of the year: ‘Pain’ 🥊, When the Fed-sponsored market beatings will end 📈, and The market beatings will continue until inflation improves 🥊.

Upgrade to paid

2. The economy is less likely to go into recession 💪

I can’t pinpoint exactly when the consensus among economists was that the U.S. was due for a recession. The worries certainly intensified after we learned GDP growth was negative in Q1 of last year, and they got a whole lot worse when we learned growth was negative in Q2 as well.

For more on how recessions are and aren’t defined, read: You call this a recession? 🤨.

Over this period, I’ve been skeptical of the idea that the U.S. was destined for a downturn given the massive economic tailwinds I couldn’t stop thinking about and still can’t stop thinking about.

Coming into 2023, the baseline expectation for many Wall Street firms was that the U.S. would enter a recession at some point during the year.

But after the robust January jobs report and expansionary January ISM Services survey earlier this month, sentiment among economists has shifted a bit.

On Monday, Goldman Sachs economist Jan Hatzius published a note titled, “Receding Recession Risk,“ in which he lowered the odds of the U.S. entering a recession in the next 12 months to 25% from 35%.

“Continued strength in the labor market and early signs of improvement in the business surveys suggest that the risk of a near-term slump has diminished notably,“ Hatzius wrote.

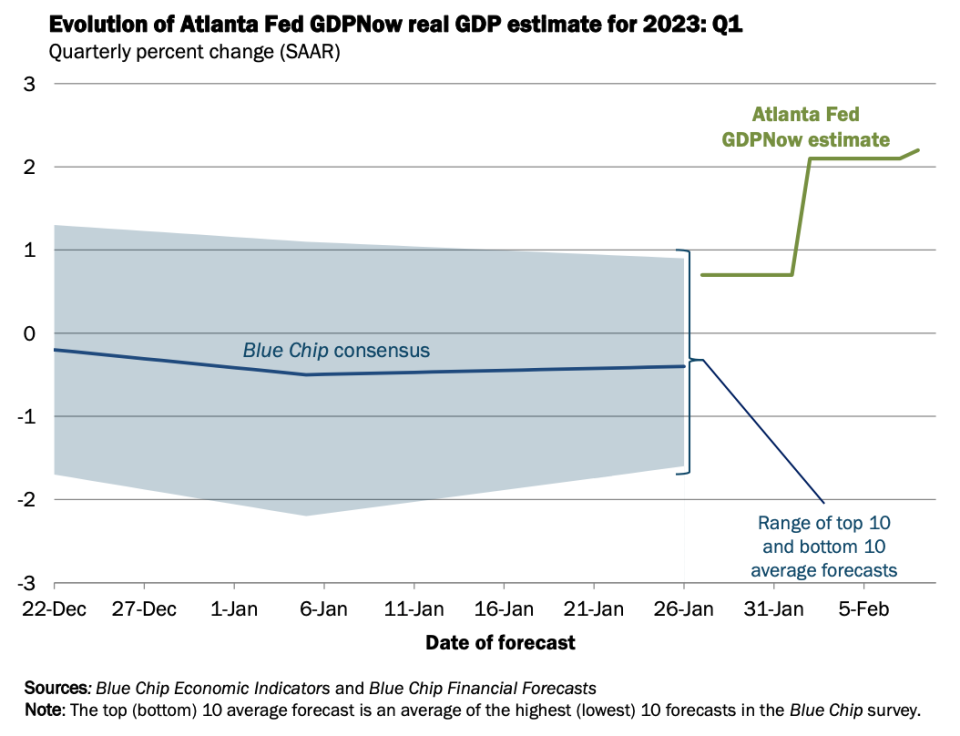

On Wednesday, we learned the Atlanta Fed’s GDPNow model saw real GDP growth climbing at a 2.2% rate in Q1. This metric is up considerably from its initial estimate of 0.7% growth as of January 27.

On Thursday, The New York Times published an article from Jeanna Smialek titled: “What Recession? Some Economists See Chances of a Growth Rebound.“ The title speaks for itself.

On Sunday, The Wall Street Journal published an article from Nick Timiraos titled: “Hard or Soft Landing? Some Economists See Neither if Growth Accelerates.“ It addresses the same themes.

All that said, it could take a few more weeks of resilient economic data before more economists officially revise their forecasts to the upside.

For more, read: 9 reasons to be optimistic about the economy and markets 💪 and The bullish ‘goldilocks’ soft landing scenario that everyone wants 😀.

3. The stock market might not crater in the first half 📉

Many prominent Wall Street strategists warned that the S&P 500 was likely to sell-off sharply during the early part of 2023 before recovering at least some of those losses later in the year. This was driven by the expectation that expectations for earnings would continue to get revised lower.

But there were at least three issues with all this: 1) stocks often rise in years when earnings fall, 2) stocks usually bottom before earnings bottom, and 3) when many people expect stocks to sell-off for the same reason, then that information is likely to be already priced into the market.

The S&P 500 is up 6.5% in 2023 so far, and the index has spent much of this period higher than where it started the year.

At least one top strategist has abandoned his call for an early sell-off. Here’s Goldman Sachs’ David Kostin in a Feb. 3 note to clients (emphasis added):

Recent macro developments have strengthened our economists’ confidence in a soft landing and reduced equity downside risk in the near term. Outside the US, the growth picture in China has brightened following an earlier-than-expected reopening and Europe is now on track to avoid a recession following a warmer-than-expected winter. In addition, Fed Chair Powell this week did little to push back on the easing of financial conditions. Our rates strategists’ expected path of Treasuries suggest little near-term upside to yields. We therefore believe the risk of a substantial drawdown in the near term has diminished, barring unforeseen data surprises. We raise our 3-month S&P 500 price target to 4,000 (-3% from today) from 3,600. As shown this week, still-light institutional investor positioning points to the risk of a chase that would see the market temporarily overshoot our S&P 500 target of 4,000.

Most of the S&P 500 have announced quarterly financial results in recent weeks, and based on what they’ve revealed, it looks like the outlook for earnings may not be as grim as previously anticipated.

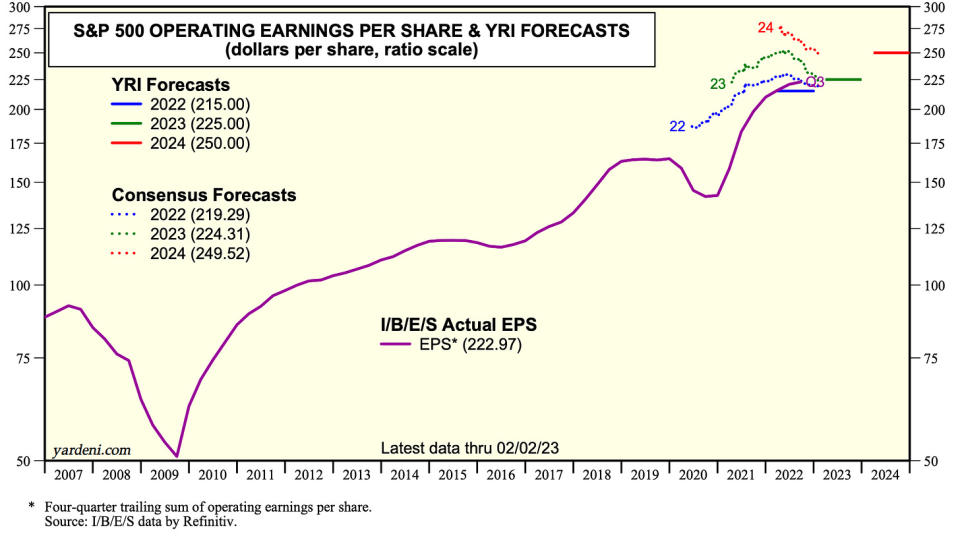

“[W]e see no recession ahead in the broad economy — or in earnings — but a soft landing,” Ed Yardeni, president of Yardeni Research, said on Tuesday (h/t Carl Quintanilla). “We are currently estimating that S&P 500 operating earnings will be up 4.7% this year to $225 per share and 11.1% next year to $250.”

The S&P 500 is currently trading above most strategists’ year-end target for the index. Should these gains hold and perhaps improve, we could soon see some strategists revise up their targets.

For more, read: Wall Street’s 2023 outlook for stocks 🔭, Stocks often rise in years when earnings fall 🤯, One of the most frequently cited risks to stocks in 2023 is ‘overstated’ 😑, and Everyone’s talking about a near-term sell-off. A contrarian signal?

What to make of all this

Not everyone thinks resilient economic growth is unambiguously good news.

“With very strong job growth, a higher labor force participation rate, and a decline in the unemployment rate to the lowest level since 1969, it is beginning to look more like a ‘no landing’ scenario,” Apollo’s Torsten Slok wrote in a February 4 note. “Under the no landing scenario the economy does not slow down, and upside risks to inflation are coming back after the initial decline in inflation driven by supply chain improvements.”

Renewed concerns about inflation could force the Fed to get more hawkish, which puts economic growth and rising stock prices at risk. In other words, good news could become bad news once again. For more on this dynamic, read: Your guide to ‘good news is bad news’ and ‘bad news is good news’ 🙃.

But if there’s one thing we’ve learned in recent months, it’s that we can simultaneously have consecutive months of healthy job growth and inflation readings that come in cool. For more on this dynamic, read: The bullish ‘goldilocks’ soft landing scenario that everyone wants 😀.

As always, time will tell what actually happens. But for the time being, the optimists appear to be triumphing over the pessimists as inflation, economic growth, and stock prices have been trending favorably in recent months.

–

More from TKer:

That’s interesting! 💡

Did you know cricket is the second most watched sport in the world? And it’s emerging in the U.S. in a big way. From JohnWallStreet:

…American Cricket Enterprises (ACE), the entity operating Major League Cricket (MLC), has raised more than $100 million. ACE founders Sameer Mehta, Vijay Srinivasan, Satyan Gajwani and Vineet Jain — and the balance of company investors — are betting the league will be able to draw the sport’s top players and attract interest from fans around the globe, becoming a staple of the cricket calendar in the process. If it can, club valuations will “grow like a hockey stick,” Sanjay Govil (chairman, Infinite Computer Solutions and CEO, Zyter Inc.) said. Govil owns the team in Washington D.C. Dallas, San Francisco, Los Angeles, New York City and Seattle will also have clubs playing in the inaugural ’23 season, which is slated to take place from June 13-30.

Reviewing the macro crosscurrents 🔀

There were a few notable data points from last week to consider:

⛓️ Supply chains continue to improve. The New York Fed’s Global Supply Chain Pressure Index

— a composite of various supply chain indicators — fell in January and is hovering at levels seen in late 2020. It’s way down from its December 2021 supply chain crisis high.

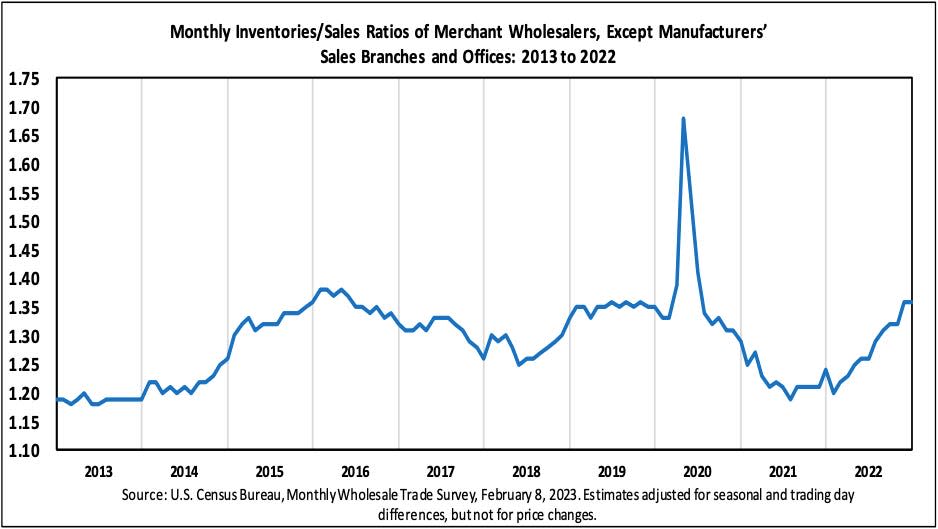

📈 Inventory levels are up. According to Census Bureau data released Tuesday, wholesale inventories climbed 0.1% to $932.9 billion in December. The inventories/sales ratio was 1.36, up significantly from 1.24 the previous year.

For more on supply chains and inventory levels, read: “We can stop calling it a supply chain crisis ⛓,“ “9 reasons to be optimistic about the economy and markets 💪, “and “The bullish ‘goldilocks’ soft landing scenario that everyone wants 😀.“

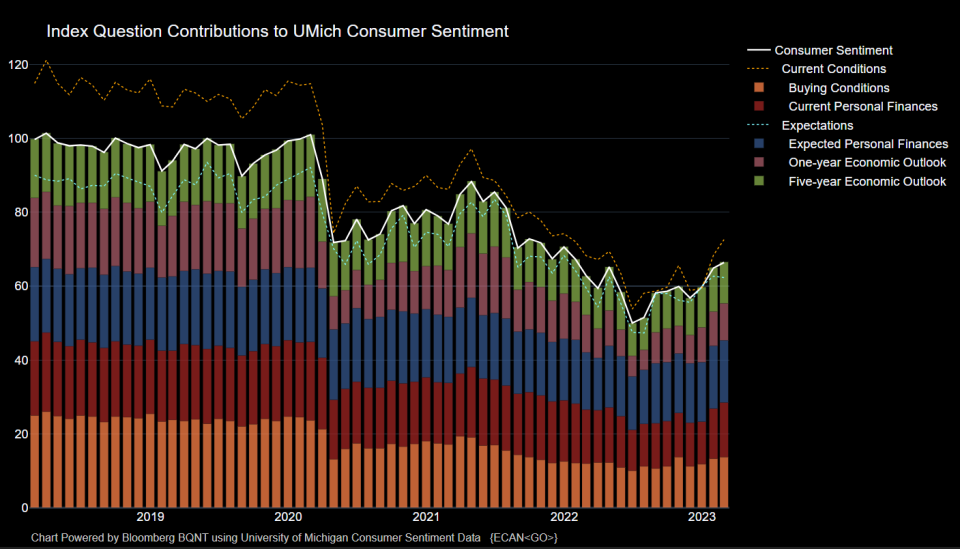

👍 Consumer sentiment is improving. From the University of Michigan February Survey of Consumers: “After three consecutive months of increases, sentiment is now 6% above a year ago but still 14% below two years ago, prior to the current inflationary episode. Overall, high prices continue to weigh on consumers despite the recent moderation in inflation, and sentiment remains more than 22% below its historical average since 1978.“

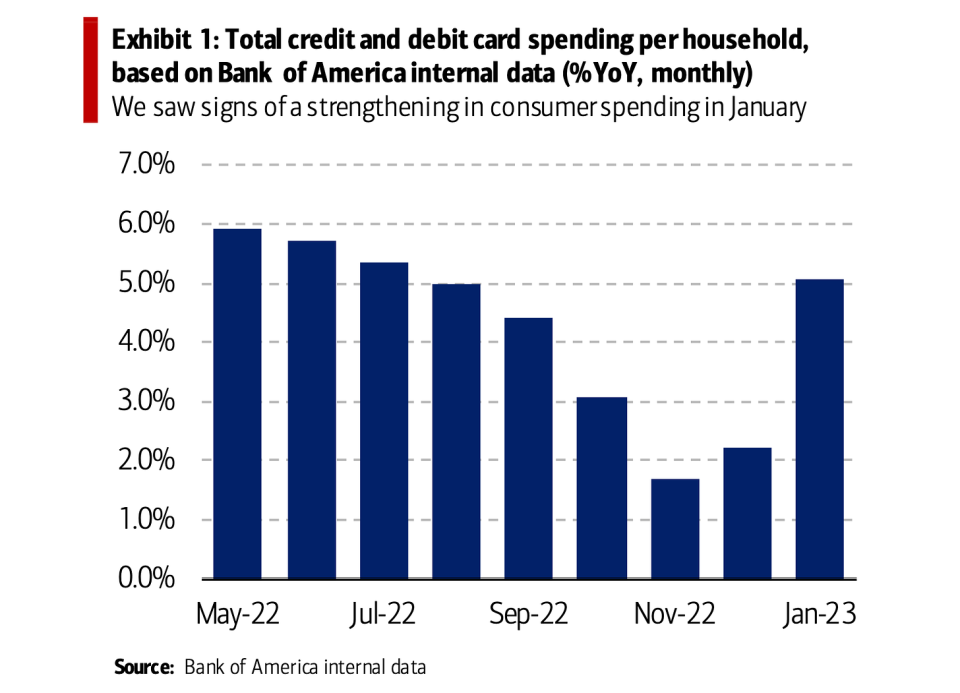

🛍️ Consumers are spending. From BofA: “We saw signs of strengthening in consumer spending in both retail and services in January, accelerating from December. Total Bank of America credit and debit card spending per household was up 5.1% YoY in January, vs. 2.2% YoY in December. On a month-over-month (MoM) seasonally adjusted (SA) basis, total card spending per household was up 1.7%, more than reversing the 1.4% MoM decline in December.“

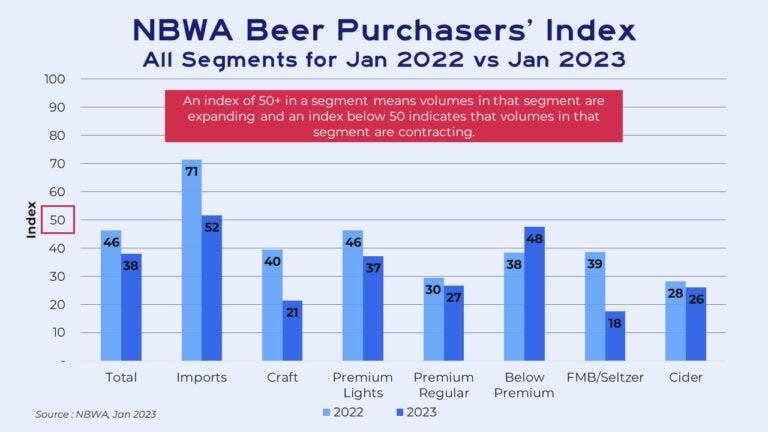

🍻 They’re buying cheap beer. From FreightWaves’ Rachel Premack: “…Beer became suddenly pricey at the end of last year. Beer prices at retail, which doesn’t include bars or restaurants, popped 7% during the last 13 weeks of 2022… That price increase is showing up in how people are buying brews, said Dave Williams, vice president of Bump Williams Consulting. People are increasingly buying, say, 12-packs over 30-packs or even single servings of beer. They’re trading down too — snagging the more economic Keystone over comparatively pricey Coors. That explains why the “below premium” segment was the only one to see an increase in demand in January compared to January 2022, according to the National Beer Wholesalers Association’s Beer Purchasers’ Index…”

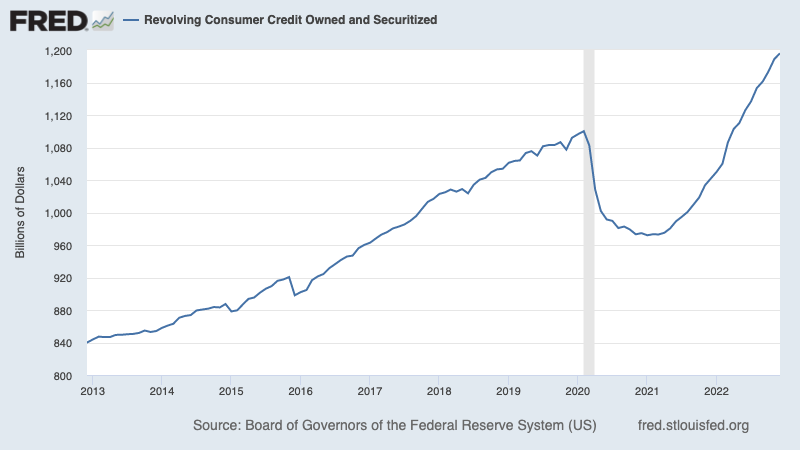

💳 Consumers are taking on more debt, but levels are manageable. According to Federal Reserve data, total revolving consumer credit outstanding increased to $1.196 trillion in December. Revolving credit consists mostly of credit card loans.

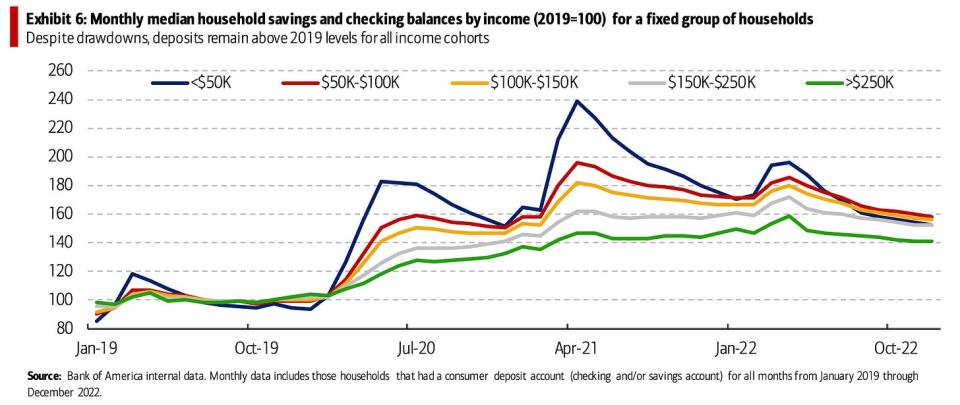

While the aggregate borrowing seems high, they’re much more reasonable when you look at consumer finances more holistically. From BofA: “On the savings side, Bank of America internal data suggests median household savings and checking balances across income groups have been trending down since April 2022, with the lowest income group (<$50k) seeing the steepest drawdown. But deposits remain above 2019 levels (Exhibit 6) for all income cohorts.“

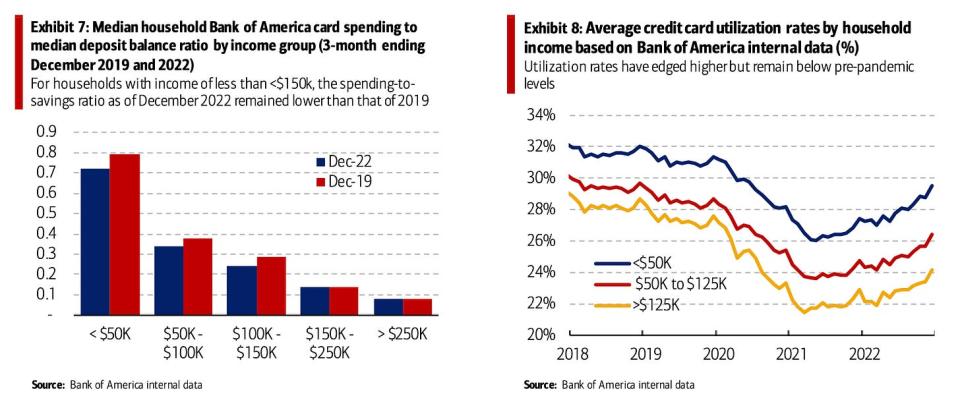

💳 No, they are not maxing out their credit cards. From BofA: “Lower income consumers appear to still have some level of comfort in terms of their financial constraints. On the one hand, the ratio of median household card spending to median deposit balances (spending-to-savings ratio) remained lower than in 2019 for households with an annual income of less than <$150k (Exhibit 7). This suggests this cohort’s spending would not need to be reduced too much for the spending-to-savings ratio to return to 2019 levels. On the other hand, the Bank of America credit card utilization rate also remained lower than in 2019 across income groups (Exhibit 8).“

For more on this, read: Consumer finances are in remarkably good shape 💰

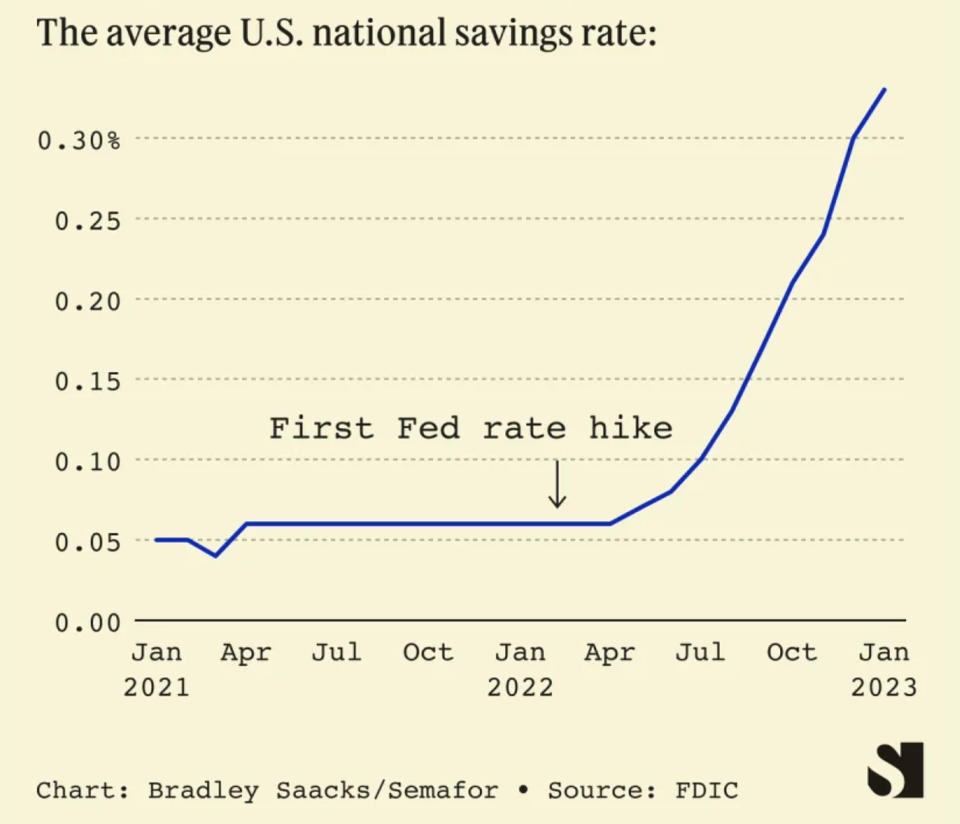

💵 Consumers are getting more on their savings accounts. From Semafor’s Liz Hoffman: “The average savings account rate has quintupled since last January to 0.33%, according to data from the U.S. Federal Deposit Insurance Corporation…“

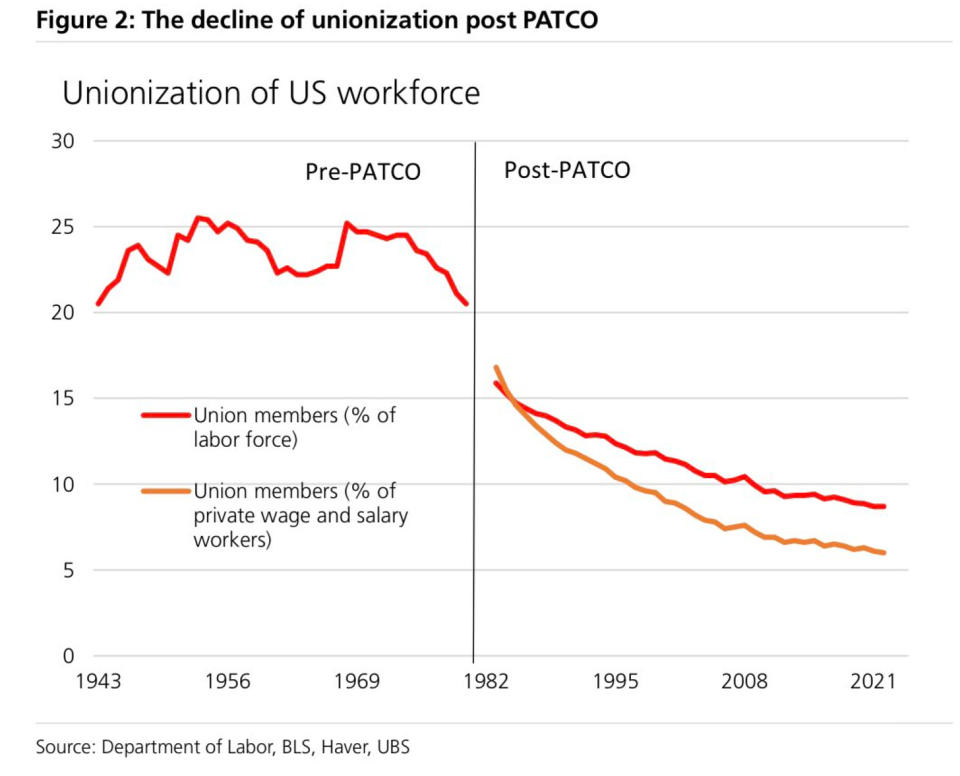

🤔 Low union participation helps explain low wage growth. From UBS: ““Wage growth is slowing noticeably along multiple measures even with a decades low unemployment rate. Why? … One reason could be low bargaining power for workers… The share of unionized workers among private employees fell to 6% in 2022, according to the BLS.”

💰 Wall Street is busy. From Bloomberg on Tuesday: “About seven IPOs are expected to raise a combined $900 million and begin trading by Friday [Feb. 10], making for the busiest week since October’s $990 million listing by Intel Corp.’s self-driving technology unit Mobileye Global Inc., according to data compiled by Bloomberg. [Last] week’s debuts include solar power equipment maker Nextracker Inc., which plans to raise as much as $535 million in what would be the year’s biggest deal yet. Enlight Renewable Energy Ltd., which is already public in Israel, plans to add a listing on the Nasdaq.“

And it’s not just IPOs. There were numerous reports of dealmaking activity last week involving some big names (link).

📉 👎 Big companies announce layoffs. On Monday, Bloomberg reported that Dell Technologies would be “eliminating about 6,650.“ On Tuesday, Zoom announced it would “say goodbye to around 1,300 hardworking, talented colleagues.“ On Wednesday, Disney announced it would be “reducing our workforce by approximately 7,000 jobs.“ On Thursday, News Corp announced “an expected 5% headcount reduction, or around 1,250 positions,” and Axios reported that Yahoo would lay off “more than 1,600 people.”

Here’s UBS economist Paul Donovan offering some perspective: “Another company—Disney this time — has announced headcount reductions. We get US initial jobless claims data [Thursday], and the macroeconomic data does not match the high profile press releases of job losses. A major reason is that large companies are not that important economically — smaller businesses matter most to labor markets. Smaller businesses tend to have underemployment rather than unemployment. It is quite hard to fire 10% of a three-person company.“

For more on this, read: Making sense of conflicting news on the labor market 🤔.

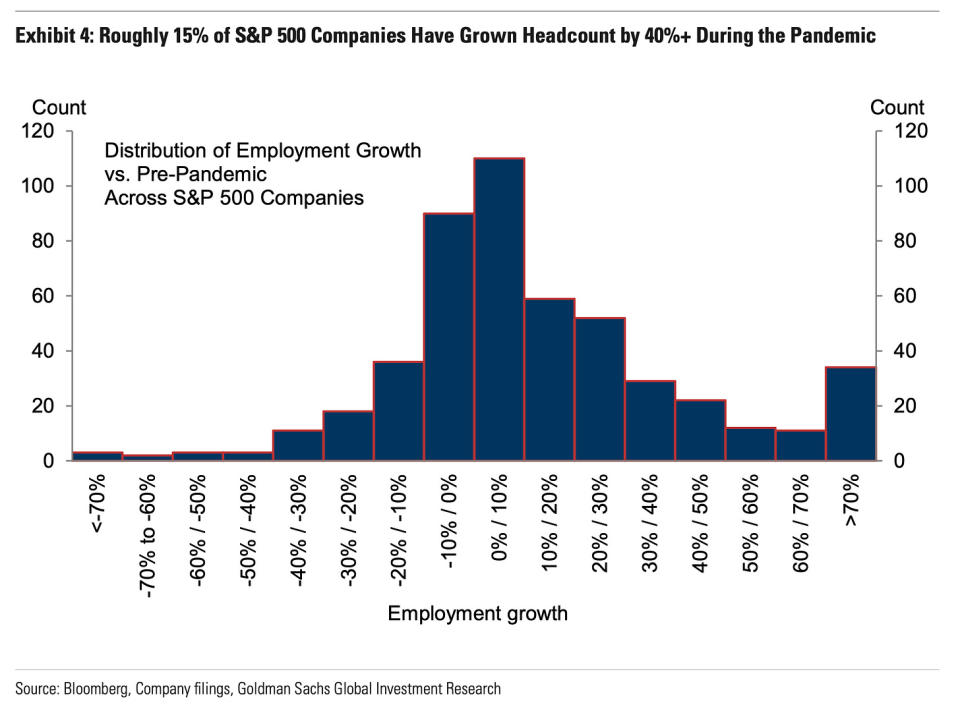

⚠️ More big layoff announcements to come? Goldman Sachs economists think it’s possible. From a research note published Monday: “…on the negative side, there could be additional layoff announcements yet to come from other large companies, as roughly 15% of companies in the S&P 500 have seen headcount increases of 40% or more since the start of the pandemic (Exhibit 4), and only one-fifth of them have announced layoffs so far.“

But: “…on the positive side, similar to the rebalancing seen so far in the broader labor market, even these companies that have announced layoffs have reduced their total demand for workers overwhelmingly by reducing job openings rather than by conducting layoffs.“ For more on job openings, read: How job openings explain everything in the economy and the markets right now 📋.

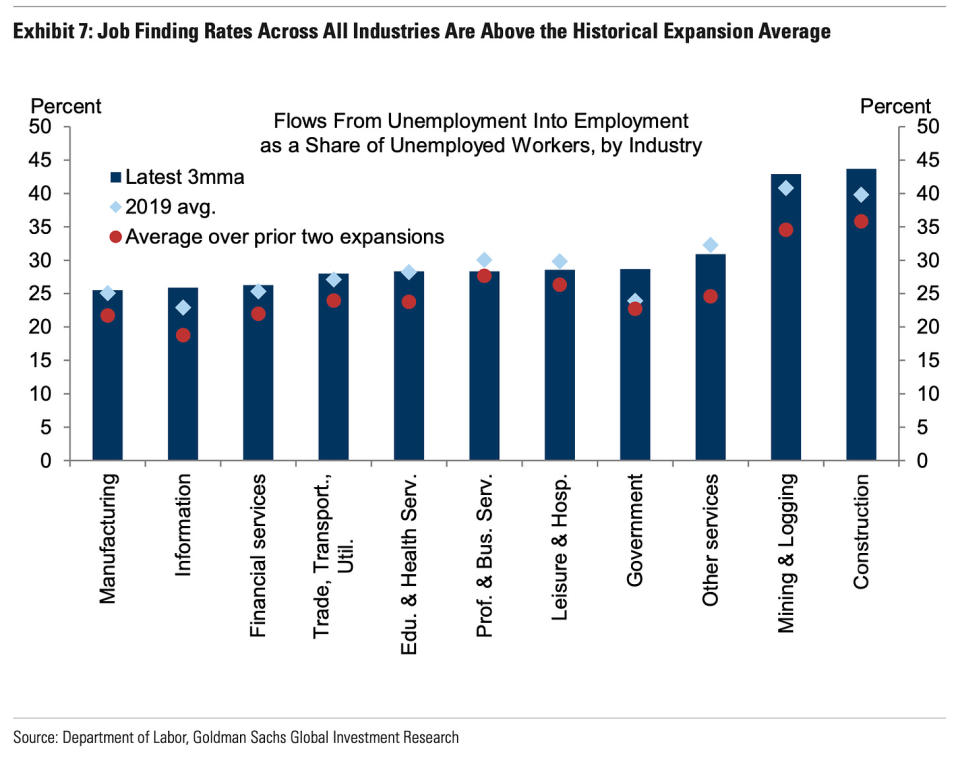

Also: “…Exhibit 7 shows that most industries (8 out of 11) have reemployment rates above pre-pandemic levels, including the information sector (the sector of most major tech companies), and that all of them have reemployment rates that are above the recent expansion average.”

I’ve started an informal thread on Twitter tracking anecdotes of companies hiring (Link).

For more on hiring, read: That’s a lot of hiring 🍾 and You should not be surprised by the strength of the labor market 💪.

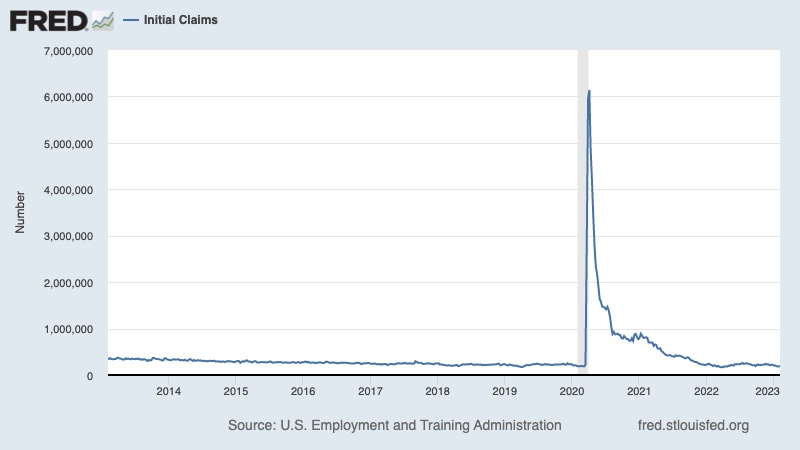

💼 Unemployment claims remain low. Initial claims for unemployment benefits climbed to 196,000 during the week ending Feb. 4, up from 183,000 the week prior. While the number is up from its six-decade low of 166,000 in March, it remains near levels seen during periods of economic expansion.

For more on low unemployment, read: 9 reasons to be optimistic about the economy and markets 💪.

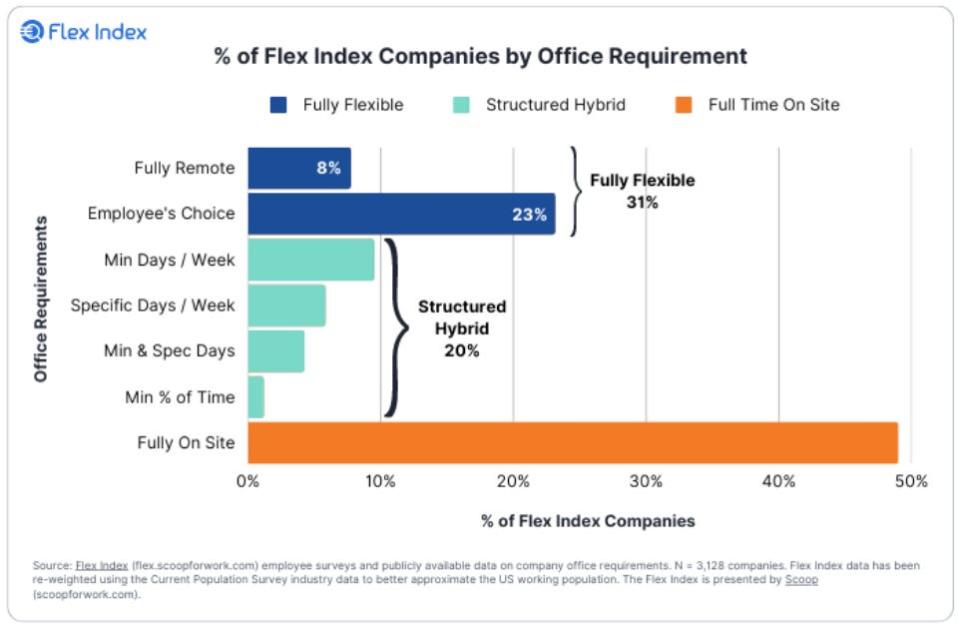

🏠 On work from home #WFH. From Stanford professor Nick Bloom: “Data on 4,000 U.S. firms #WFH policies: 1) 50% of firms are fully on-site, like food-service, accommodation and retail, 2) 40% combine #WFH and in person days in various ways: min-days, anchor days, employee choice etc, 3) 8% are fully remote“

Putting it all together 🤔

We’re getting a lot of evidence that we may get the bullish “Goldilocks” soft landing scenario where inflation cools to manageable levels without the economy having to sink into recession.

And the Federal Reserve has recently adopted a less hawkish tone, acknowledging on February 1 that “for the first time that the disinflationary process has started.“

Nevertheless, inflation still has to come down more before the Fed is comfortable with price levels. So we should expect the central bank to continue to tighten monetary policy, which means we should be prepared for tighter financial conditions (e.g. higher interest rates, tighter lending standards, and lower stock valuations). All of this means the market beatings may continue and the risk the economy sinks into a recession will be elevated.

It’s important to remember that while recession risks are elevated, consumers are coming from a very strong financial position. Unemployed people are getting jobs. Those with jobs are getting raises. And many still have excess savings to tap into. Indeed, strong spending data confirms this financial resilience. So it’s too early to sound the alarm from a consumption perspective.

At this point, any downturn is unlikely to turn into economic calamity given that the financial health of consumers and businesses remains very strong.

As always, long-term investors should remember that recessions and bear markets are just part of the deal when you enter the stock market with the aim of generating long-term returns. While markets have had a terrible year, the long-run outlook for stocks remains positive.

For more on how the macro story is evolving, check out the previous TKer macro crosscurrents »

For more on why this is an unusually unfavorable environment for the stock market, read: The market beatings will continue until inflation improves 🥊 »

For a closer look at where we are and how we got here, read: The complicated mess of the markets and economy, explained 🧩 »

This post was originally published on TKer.co

Sam Ro is the founder of TKer.co. Follow him on Twitter at @SamRo

Click here for the latest stock market news and in-depth analysis, including events that move stocks

Read the latest financial and business news from Yahoo Finance

Download the Yahoo Finance app for Apple or Android

Follow Yahoo Finance on Twitter, Facebook, Instagram, Flipboard, LinkedIn, and YouTube

[ad_2]

Source link