Oppenheimer Says This Sector Is an Attractive Place to Be

[ad_1]

Markets move in cycles, some large, some small. 2021 saw a strong bullish trend, the strongest in decades; it was followed by a strong bearish trend, the strongest in decades, in 2022. This year opened with a turn back up that lasted through most of January. And in February, there was a pause. A brief pause, likely, before we start the next leg up, at least according to Oppenheimer chief technical strategist Ari Wald.

Wald notes that the S&P 500 has reversed last year’s bear run, and that despite volatility so far this month that reversal remains intact above 3,950. In fact, the S&P 500 index stands now at 4,137 and is pointing back upwards.

“While we expect the bull market to continue,” Wald says, “we reiterate it won’t be a straight line higher, either. Still, the point is that investors should be thinking in terms of buying weakness rather than selling strength, in our view. With top-down headwinds easing, we also recommend placing greater emphasis on identifying emerging relative strength, and less emphasis on market timing. With this in mind, we make the case that the Financials sector is positioned to lead the next leg of the advance.”

Getting into details, Wald adds, “Capital Markets is our top industry idea for Financials sector exposure based on its long-term trend of higher relative lows since 2012. The industry is supported by broader internal breadth and is closer to a relative breakout too, by our analysis.”

Against this backdrop, we’ve used the TipRanks database to pull up details on two stocks, from the Capital Markets industry, that Oppenheimer has tapped as Top Ideas for 2023. Are these the right stocks for your portfolio? Let’s take a closer look.

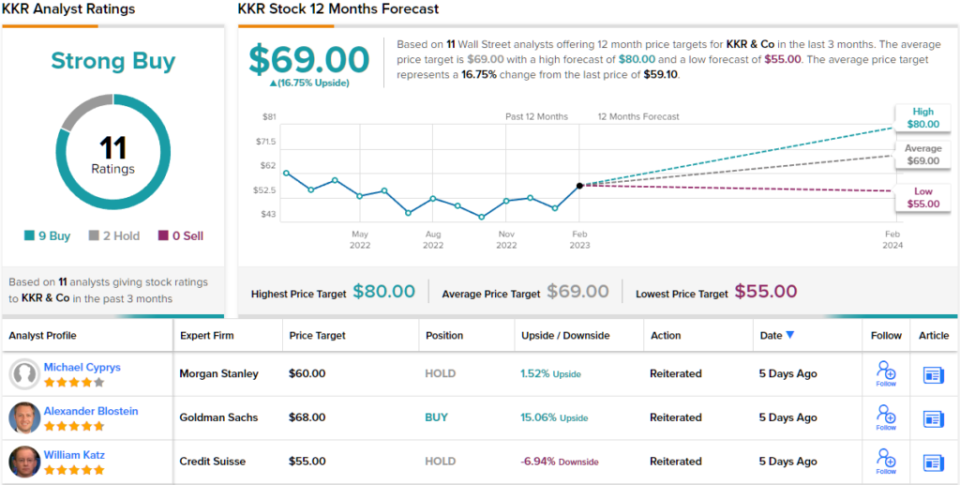

KKR & Co. Inc. (KKR)

The first Oppenheimer pick we’re looking at is KKR, a global investment and asset management firm, offering services to a world-wide clientele. KKR follows a model that brings third-party capital into connection with the capital markets business, giving the resources to do everything from taking companies through the process of going public to underwriting new market deals to investing in debt and equity. The company mobilizes long-term capital into these purposes, generating solid returns over time for fund investors and stockholders.

As of the end of 4Q22, the company had over $504 billion in total assets under management, up from $470.6 billion a year before. The asset management portfolio brought in over $693 million in revenue, with another $1.835 billion coming from the insurance service segment, for a total GAAP revenue of $2.53 billion for the quarter. This was down from $4.05 billion in the same quarter last year, but topped Wall Street expectations of $1.41 billion. The company remains solidly profitable, as adj. EPS came in at $0.92, trumping the Street’s call for $0.85.

Overall, KKR finished 2022 with sound capital metrics. The company had $108 billion in uncalled commitments, representing capital available for deployment, and even thought last year was a difficult economic environment, KKR raised $16 billion in capital during 2022.

In his coverage of this stock for Oppenheimer, 5-star analyst Chris Kotowski continues to take an upbeat stance on KKR’s prospects despite the challenges ahead. He writes, “We’re not out of the clear just yet as challenges remain from the 2022 backdrop; however, we find ourselves with continued confidence in the KKR engine given its resilience on all fronts (fundraising, deployment, performance) and ongoing, balance-sheet bolstered flexible growth—both organic and strategic… We continue to think KKR is a very compelling investment.”

Kotowski goes on to reiterate his Outperform (i.e. Buy) rating on KKR shares, and his $80 price target implies a one-year gain of 35% waiting in the wings. (To watch Kotowski’s track record, click here)

Overall, KKR shares have a Strong Buy rating from the analyst consensus, showing that Wall Street agrees with Kotowski’s assessment. The rating is based on 9 Buys and 2 Holds set in the past 3 months. (See KKR stock forecast)

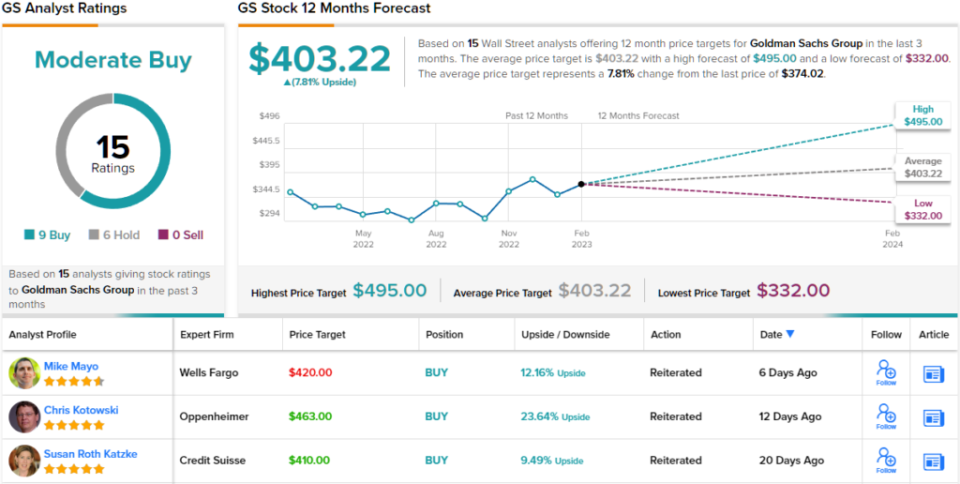

Goldman Sachs Group (GS)

The next stock we’re looking at is one of the major names in banking, the Goldman Sachs Group. GS is an international bank holding company, one of listed firms on the Dow Jones Industrial Average, and a big-name player in trading and investments, asset management, and securities services. Goldman mainly serves other institutions, such as banks, corporations, and governments, but has been known to take on small numbers of individual clients with ultra-high net worth.

In last month’s financial release for Q4 and full year 2022, the bank reported year-over-year drops in both revenues and earnings. Starting at the top line, Goldman had $10.59 billion in revenue, down 16% from the prior year quarter. At the bottom line, earnings plunged 66% from a year earlier to $1.33 billion, or $3.32 per share. Both figures missed Street expectations.

Common shareholders, however, have not done too badly. Goldman maintained an ROE of 10.2% for all of 2022 and 4.4% for Q4; these numbers can be compared to 11% and 4.8% from the prior year. All in all, in a year buffeted by high inflation and rising interest rates, GS shares brought a sound return to investors.

Oppenheimer’s Chris Kotowski sees returns on equity has a key point here, writing: “Even if a slow investment banking environment persists, we would expect GS to maintain a double-digit ROTCE and think the stock is oversold at just 1.2x tangible book… Goldman’s relatively new senior management team has embarked on a series of initiatives to raise ROTE, which has averaged roughly 11% in recent years, to at least 15%. We think this effort has a strong possibility of success because the company has a strong franchise and there are multiple revenue, cost, and capital optimization strategies that can be implemented, but the market is still valuing the stock as though the returns will remain unchanged indefinitely.”

Looking ahead, Kotowski sets an Outperform (i.e. Buy) rating on GS shares, along with a $441 price target that suggests a one-year upside potential of ~24%.

So we have one 5-star analyst coming out for the bulls on this one – but what does the rest of the Street make of GS’s prospects? The stock has picked up 15 recent analyst reviews, and they include 9 Buys and 6 Holds, for a Moderate Buy consensus view. (See Goldman Sachs stock forecast)

To find good ideas for stocks trading at attractive valuations, visit TipRanks’ Best Stocks to Buy, a tool that unites all of TipRanks’ equity insights.

Disclaimer: The opinions expressed in this article are solely those of the featured analysts. The content is intended to be used for informational purposes only. It is very important to do your own analysis before making any investment.

[ad_2]

Source link